Comments Off on Prediction addiction: Do you suffer from it?

Robin writes:

I believe it was Jason Zweig from the Wall Street Journal who coined the phrase prediction addiction. Whoever came up with it, the term helps to explain why so many people earn lower investment returns than they should.

Of course, prediction addiction isn’t confined to the investing arena. We love to predict the outcomes of everything from elections to sporting events, and, of course, gambling has become a multi-billion-pound industry worldwide.

Behavioural scientists tell us this drive to predict the future stems from a complex interplay of evolutionary, cognitive and socio-cultural factors. For example:

humans have a strong desire for control and certainty;

our brains are wired to recognise patterns, even where they don’t exist:

confirmation bias leads us to ignore information that doesn’t support our predictions, which leads to overconfidence;

optimism bias can encourage us to predict and shape a more favourable future;

and the world, and predicting the future is a way of extending the narratives we like to create about our lives and the world; and

societal and cultural norms often encourage future planning, emphasising the importance of being “ahead of the game”.

There is abundant evidence that this desire to predict and to gamble has an impact on the many people invest their money. In a 2011 survey, for example, 41% of high-net-worth investors around the world said they wished they were more disciplined in their investment decision-making.

I don’t want to sound puritanical about this. As the behavioural finance expert Meir Statman has explained, investing provides “expressive and emotional benefits” as well as financial ones. Some investors see picking stocks stocks and funds and trying to time the market as a hobby, while others, let’s face it, just enjoy a flutter.

However, as I explain in this, the first of a new series of articles for Index Fund Advisors in California, there is a price to pay for prediction addiction in terms of investment performance. For some it can be significant.

Thankfully, if you’re addict yourself or fear you’re becoming one, there are steps you can take to reassert control over your investment decision-making.

So what do you you think of this content? Follow us on social media and join the debate. We would love to hear your views. We’re on Twitter, LinkedIn and YouTube.

Comments Off on Testing the patience of value investors

By LARRY SWEDROE

Patience: A quality apparent among such lower life forms as snails and tortoises but rarely among humans who invest in financial assets.

— Jason Zweig, The Devil’s Dictionary

The decade from 2012 through 2021 provided a test of the faith and discipline for value investors as the Fama-French U.S. Growth Research Index outperformed the Fama-French U.S. Value Research Index by 4.6 percentage points per year (19.3 percent versus 14.7 percent), with most of that underperformance occurring during the four years from 2017 to 2020, when the Growth Research Index outperformed by 18.4 percentage points (23.8 percent versus 5.4 percent). Unfortunately, such long periods of underperformance led many investors to ignore the long-term evidence —from 1927 through 2021, the Fama-French Value Research Index outperformed the Fama-French Growth Research Index, 12.8 percent versus 10.2 percent. Note that while growth stocks are typically far more profitable than value stocks and they grow faster—which is why they deservedly command premium multiples — they have underperformed value stocks over the long term. The failure to consider that the price you pay for that faster growth (meaning the discount rate applied to future earnings) matters a great deal, along with the failure to consider the long-term historical return evidence, causes many to lose faith, believing the notion that “this time it’s different” and there’s a “new normal” in which innovative, disruptive growth companies will outperform value companies.

To help value investors keep the faith, we’ll review some important facts that show that the source of growth’s outperformance over 2012-2021 had very little to do with growth companies generating greater than already expected financial performance. We’ll begin by reviewing the findings from the 2021 study Reports of Value’s Death May Be Greatly Exaggerated. The authors found that virtually all the outperformance of growth stocks as far back as 2007 was due to a widening of the spread in P/E ratios between growth and value stocks. They also found that there was little difference in overall profitability of growth and value, as the average return on equity difference was almost the same before and after 2007 — there was no new normal or we would have seen a widening in profitability.

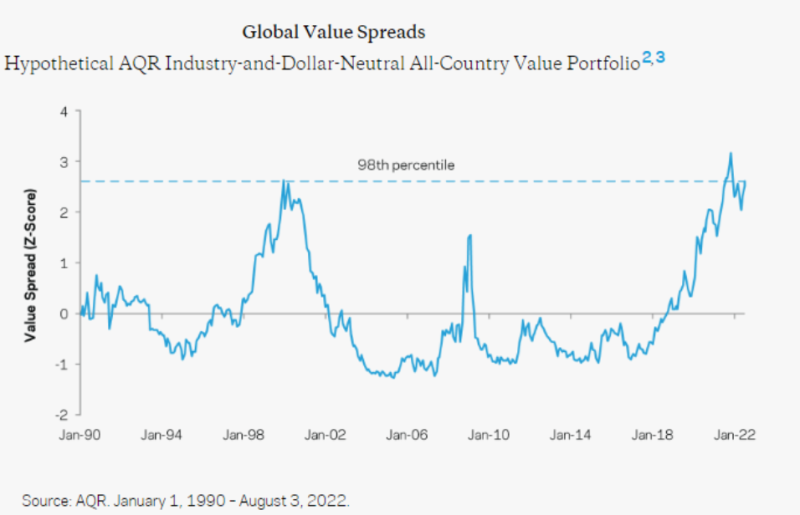

The good news for those patient value investors is that the outperformance of growth over the prior decade, which led to the valuation spread widening, pushed the spreads to historically high levels. Thanks to AQR Capital Management, we see that in August 2022, the spread was at the 98th percentile globally. Since the spread has been positively correlated with the future value premium, value investors should expect a higher than historical value premium going forward.

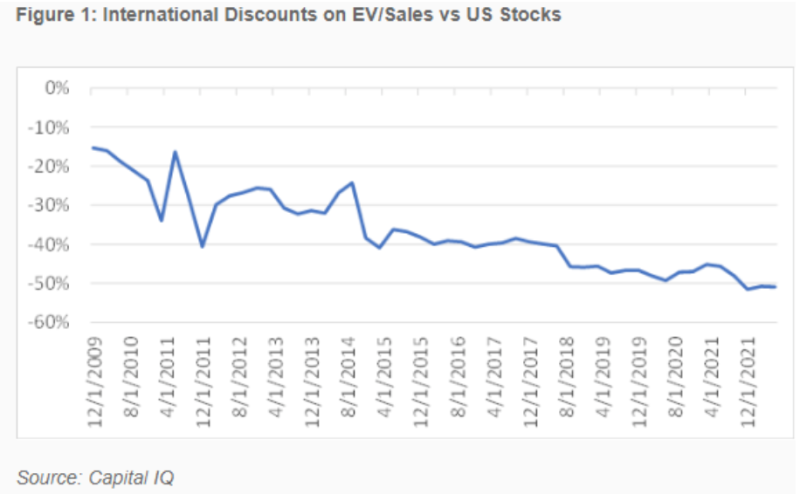

Thanks to the research team at Verdad, we can also examine other metrics that explain both value’s underperformance over the prior decade and why value investors should not lose patience. In the chart below, Verdad showed that over the past decade, international stocks went from trading at about a 15 percent discount to U.S. stocks based on enterprise value-to-sales to a 50 percent discount — international value companies were getting persistently cheaper relative to growth stocks.

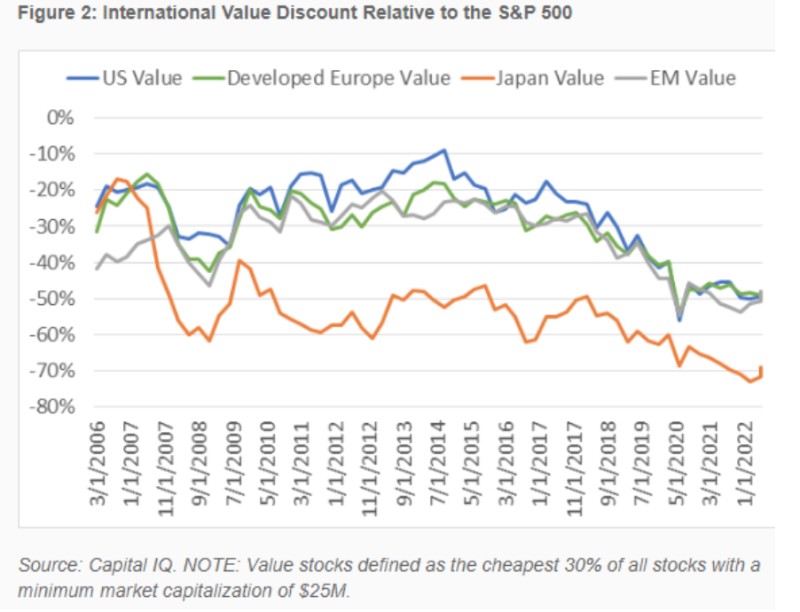

In the following chart, Verdad compared the enterprise value (EV)/EBITDA (earnings before interest, taxes, depreciation and amortisation) ratio for the cheapest 30 percent of stocks in each market to that of the S&P 500 Index. As you can see, value stocks globally “cheapened” by 20 percentage points or more over the past decade relative to the S&P 500. U.S., developed Europe, and emerging market value stocks are now trading at a 50 percent discount to the S&P 500, while Japan is trading at a 70 percent discount.

Was the widening of discounts justified?

It’s certainly possible that the widening spreads in valuations were justified by greater than expected financial performance of growth stocks relative to that of value stocks. However, as noted earlier, the authors of the studyReports of Value’s Death May Be Greatly Exaggerated found that while the difference in return on equity for growth stocks relative to value stocks had increased since 2007, the difference was minor and could not explain the difference in performance.

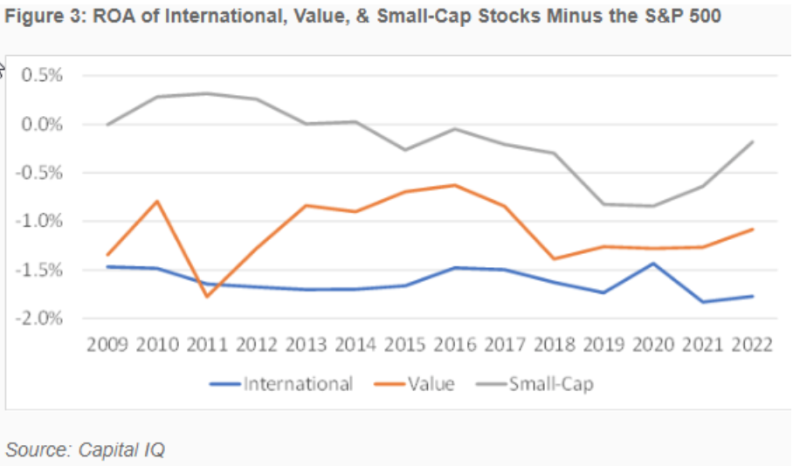

Verdad provided further evidence that greater than expected financial performance did not explain the lost decade for value stocks. In the following chart, Verdad showed the difference between the return on assets (ROAs) of the S&P 500 and international stocks (as measured by the S&P International 700), small-cap stocks (as measured by the S&P 600) and value stocks (as measured by the S&P 500 Pure Value) over the past 13 years. The chart shows that while international, value and small-cap stocks have lower ROAs on average than the broad U.S. market (explaining why the growth stocks have higher P/E ratios), the differences are small, and importantly, there was relatively little change over the period—the outperformance of U.S. growth stocks could not be explained by their greater than expected financial performance.

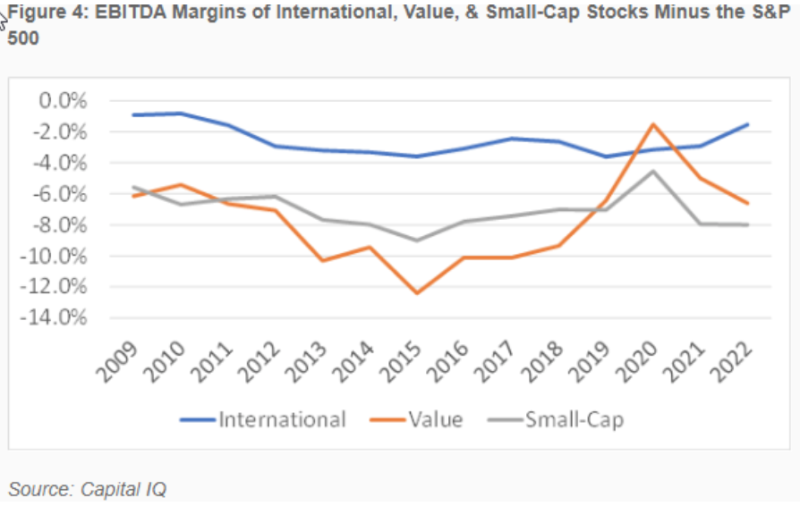

Verdad next turned to examining profit margins. The chart below shows the difference between the EBITDA margins of the S&P 500 and international stocks, small-cap stocks and value stocks (as measured by the same indexes as in Figure 3 above). As you can see, value stocks have lower margins than S&P 500 stocks, but those margin differences are relatively unchanged from a decade ago, albeit with high volatility for value stocks (the higher volatility helps explain why value stocks have lower valuations—they are riskier). Again, we see that the outperformance of growth stocks cannot be explained by financial performance that was greater than already anticipated (the EBITDA margins did not widen).

Has the tide already turned?

Signs of the end of the “new normal” in which growth stocks outperformed by wide margins began to appear in November 2020. From then through July 2022, the Fama-French U.S. Value Research Index outperformed the Fama-French U.S. Growth Research Index by 26.2 percentage points per annum (37.3 percent versus 11.1 percent).

Investor takeaways

The first takeaway is that investors should be careful when drawing conclusions based on differences in returns and make sure they understand the source of the outperformance. For example, stocks can underperform safe Treasury bills for a long time simply because the risks show up, causing the valuations of equities to fall as the risk premium demanded by investors rises. That greater risk premium should cause investors to expect higher future returns. And asset classes, like growth stocks, can outperform simply because of speculative demand, causing their relative valuations to rise as the discount rate applied to their expected future earnings falls. When that occurs, investors subject to recency bias expect that outperformance to continue. However, what they should expect is lower future returns because of the lower risk premium now demanded.

The second takeaway is that investors should be careful about drawing conclusions from relatively short data samples, and when it comes to risky assets, history suggests that 10 years of relative underperformance is likely to be nothing more than what economists call “noise,” a random outcome. If you doubt that, consider the three periods of at least 13 years over which the S&P 500 Index underperformed riskless one-month Treasury bills: 1929-43 (15 years), 1966-1982 (17 years) and 2000-12 (13 years). That is 45 of the last 93 years. Despite this, the S&P 500 Index outperformed one-month Treasury bills over the full period by 6.6 percent per annum, 9.9 percent versus 3.3 percent.

The third takeaway is that there was, and is, no new normal for growth stocks. In fact, we have “been there and done that” during the late 1990s (the dot-com era) when growth stocks outperformed because their relative valuations rose. And similar, though smaller, drawdowns for value stocks occurred during the biotech boom from 1989-1991 and the during the “Nifty Fifty” era (1969-1971). The widening of the valuation spread should have led investors to expect value to outperform by more than it had historically. And that is exactly what happened in each case. For example, the dot-com era was followed by the largest outperformance of value stocks relative to growth stocks in history. Over the eight-year period 2000-2007, the Fama-French U.S. Value Research Index returned 11.0 percent per annum, outperforming the Fama-French U.S. Growth Research Index return of just 0.4 percent per annum by 10.6 percentage points a year. As you saw in the chart on valuation spreads from AQR, today’s valuation spreads are very similar to what they were at the last peak in the “bubble” in growth stocks. While that isn’t a guarantee that value stocks will outperform, and do so by significant margins, it’s what the historical evidence suggests is likely.

If you are among the many investors considering losing your patience with value investing in favour of putting all their money in the S&P 500 or a total market fund, consider that valuation gaps that have driven wide relative return differences have historically been strongly mean reverting. The knowledge of financial history can help prevent investors from falling prey to stories of new eras and new normals and becoming victims of recency bias.

The information presented herein is for educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Certain information may be based on third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party Web sites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of the Buckingham Strategic Wealth® or Buckingham Strategic Partners® (collectively Buckingham Wealth Partners). LSR-22-379

LARRY SWEDROE is Chief Research Officer at Buckingham Strategic Wealth and the author of numerous books on investing.

Investors are far more likely to achieve their goals if they use a financial adviser. But really good advisers with an evidence-based investment philosophy are sadly in the minority.

If you would like us to put you in touch with one in your area, just click here and send us your email address, and we’ll see if we can help.

Comments Off on Your chief problem and worst enemy as an investor

By ROBIN POWELL

One of my favourite investment authors is Benjamin Graham. Widely credited as the father of value investing, Graham was Warren Buffett’s mentor and wrote the classic book, The Intelligent Investor.

One of the central themes of that book is the investor’s capacity for self-harm. “The investor’s chief problem,” Graham wrote, “and even his worst enemy, is likely to be himself.”

Jason Zweig of the Wall Street Journal reminded us this week that Graham’s warning is particularly relevant at times such as these, when global markets are volatile. What Graham teaches us, writes Zweig, is that, as an investor, “your results depend much less on how markets behave than on how you behave.”

“In recent years,” he goes on, “investors have been led to believe that their greatest asset is the ability to trade at will for free. Graham says: No way.

Not your problem

“Your basic advantage as an investor is that you don’t have to trade because everybody else is. When everybody is selling, that’s their problem; it doesn’t have to be yours.

“When the market’s behaviour doesn’t make sense to you, you don’t have to join in. You can marvel at what is going on, but you don’t have to follow the flock…

“If you sell just because other people are selling, you make yourself hostage to the whims of tens of millions of strangers who often go collectively crazy. That’s no way to live, and it’s no way to invest.”

Easier said than done

Of course, keeping your head when all around you seem to be losing theirs isn’t easy. It requires patience, discipline and emotional resilience.

But most of all, as the fourth part in our latest video series How to Invest, commissioned by Wealth Matters, explains, it requires self-knowledge.

So, invest time in getting to know yourself better. Work out the ways in which your own beliefs and personality could actually get in your way, and learn to spot the warning signs. Most importantly, make sure there’s someone you can turn to when you really need them.

Comments Off on Fama: It’s Putin who’s irrational, not the markets

By ROBIN POWELL

As most investors know, the markets hate uncertainty, and the world seems more uncertain now than it ever has done in most people’s lifetimes.

How long will we live in the shadow of Covid? Will rapidly rising prices cause a global recession? More pressingly, are we entering a long-drawn-out war in Europe? A new cold war perhaps? Or even a nuclear one?

In any other week than this one, the latest report from the UN’s Intergovernmental Panel on Climate Change would be headline news. But even the revelation that climate-related impacts are hitting the world at the high end of what modellers once expected has hardly received a mention.

We crave starkly simple views

At times like these, the human brain craves pat answers. “When the world turns upside down,” Jason Zweig recently wrote in the Wall Street Journal, “starkly simple views are reassuring. Yet it’s at those very moments that investors need to be even more sceptical about takes that smack of certainty.”

The New York Times is running an interview today with the distinguished University of Chicago economist Eugene Fama. Now aged 83 but still hard at work, Fama is asked by the NYT journalist Jeff Sommer for his views on the Ukraine crisis and what investors should make of it.

“I don’t know” features heavily

Many readers, I’m sure, will be frustrated at Fama’s answers — the phrase “I don’t know” features several times — and you can almost picture Jeff Sommer willing Fama to give him at least one or two juicy quotes. But it is, all the same, an interview that every investor should read.

If anyone should know the answers, it’s Professor Fama. He’s spent six decades studying stock market prices. Yet he’s happy to admit that he doesn’t.

That doesn’t mean, however, that we can’t learn from Fama’s wisdom on the current situation. On the contrary, Fama’s conclusion from a lifetime of study is that markets do provide answers — even if they aren’t the answers you want to hear.

Here are some of the highlights from Jeff Sommer’s interview with Eugene Fama:

It’s Putin who’s irrational

“War… isn’t rational, it’s just destruction. Take World War II. Rationally, it should never have happened. Hitler? He was irrational; of course he was. And Putin, he is irrational. Who can understand why he’s doing what he’s doing?”

Markets may be struggling to price securities…

“Basically, we’re in a period where we have had an injection of uncertainty into the world, so speculative prices are going to go up and down in response. People are continuously trying to evaluate information. But it’s impossible for them, given the amount of uncertainty that’s out there, to come up with good answers.”

…but that doesn’t mean markets are irrational

“Markets can be rational without politics being rational or people always being rational. The problem with pricing is a question of how much is knowable right now. How’s this Russia thing going to work out? Who knows?”

Fama doesn’t read the analyses of Wall Street fund houses

“I don’t read any of that. It’s investment porn.”

You can never relax about equity markets

“There is always risk in the stock market, always. It never goes away. People have to remember that.”

Markets can go into a long and deep decline

“Two decades might not be enough. In the future, it could be longer. Really, there’s no answer. You just don’t know. There’s always a risk it will take longer than your lifetime.”

Can the Fed bring inflation down without causing a recession?

“I have no idea. Unfortunately, Milton Friedman, if he were alive today, wouldn’t know either. He’d be shocked, really. He’d have to rethink everything.”

How will the Ukraine crisis play out?

“I’ve learned not to make predictions. Can’t do it. Who knows?”

ROBIN POWELL is the editor of The Evidence-Based Investor. He works as a journalist and consultant specialising in finance and investing, and as a campaigner for a fairer, more transparent asset management industry. You can find him here on LinkedIn and Twitter.

Wherever they are in the world, we will put TEBI readers in contact with an adviser in their area (or at least in their country) whom we know personally, who shares our evidence-based investment philosophy and who we feel is best able to help them. If we don’t know of anyone suitable we will say.

We’re charging advisers a small fee for each successful referral, which will help to fund future content.